This function performs correlation tests for the shocks generated by simshocks.

Arguments

- x

gaussian (bivariate) shocks, with correlation, generated by

simshocks(if Gaussian copula).- alternative

indicates the alternative hypothesis and must be one of "two.sided", "greater" or "less".

- method

which correlation coefficient is to be used for the test : "pearson", "kendall", or "spearman".

- conf.level

confidence level.

Value

a list with 2 components : estimated correlation coefficients, and confidence intervals for the estimated correlations.

References

D. J. Best & D. E. Roberts (1975), Algorithm AS 89: The Upper Tail Probabilities of Spearman's rho. Applied Statistics, 24, 377-379.

Myles Hollander & Douglas A. Wolfe (1973), Nonparametric Statistical Methods. New York: John Wiley & Sons. Pages 185-194 (Kendall and Spearman tests).

See also

Examples

nb <- 500

s0.par1 <- simshocks(n = nb, horizon = 3, frequency = "semi",

family = 1, par = 0.2)

s0.par2 <- simshocks(n = nb, horizon = 3, frequency = "semi",

family = 1, par = 0.8)

(test1 <- esgcortest(s0.par1))

#> $cor.estimate

#> Time Series:

#> Start = c(0, 2)

#> End = c(3, 1)

#> Frequency = 2

#> [1] 0.17019209 0.09279227 0.18718789 0.22185835 0.14601034 0.19899949

#>

#> $conf.int

#> Time Series:

#> Start = c(0, 2)

#> End = c(3, 1)

#> Frequency = 2

#> Series 1 Series 2

#> 0.5 0.083751429 0.2540906

#> 1.0 0.005143531 0.1790261

#> 1.5 0.101157771 0.2704393

#> 2.0 0.136829774 0.3036416

#> 2.5 0.059076143 0.2307465

#> 3.0 0.113285783 0.2817730

#>

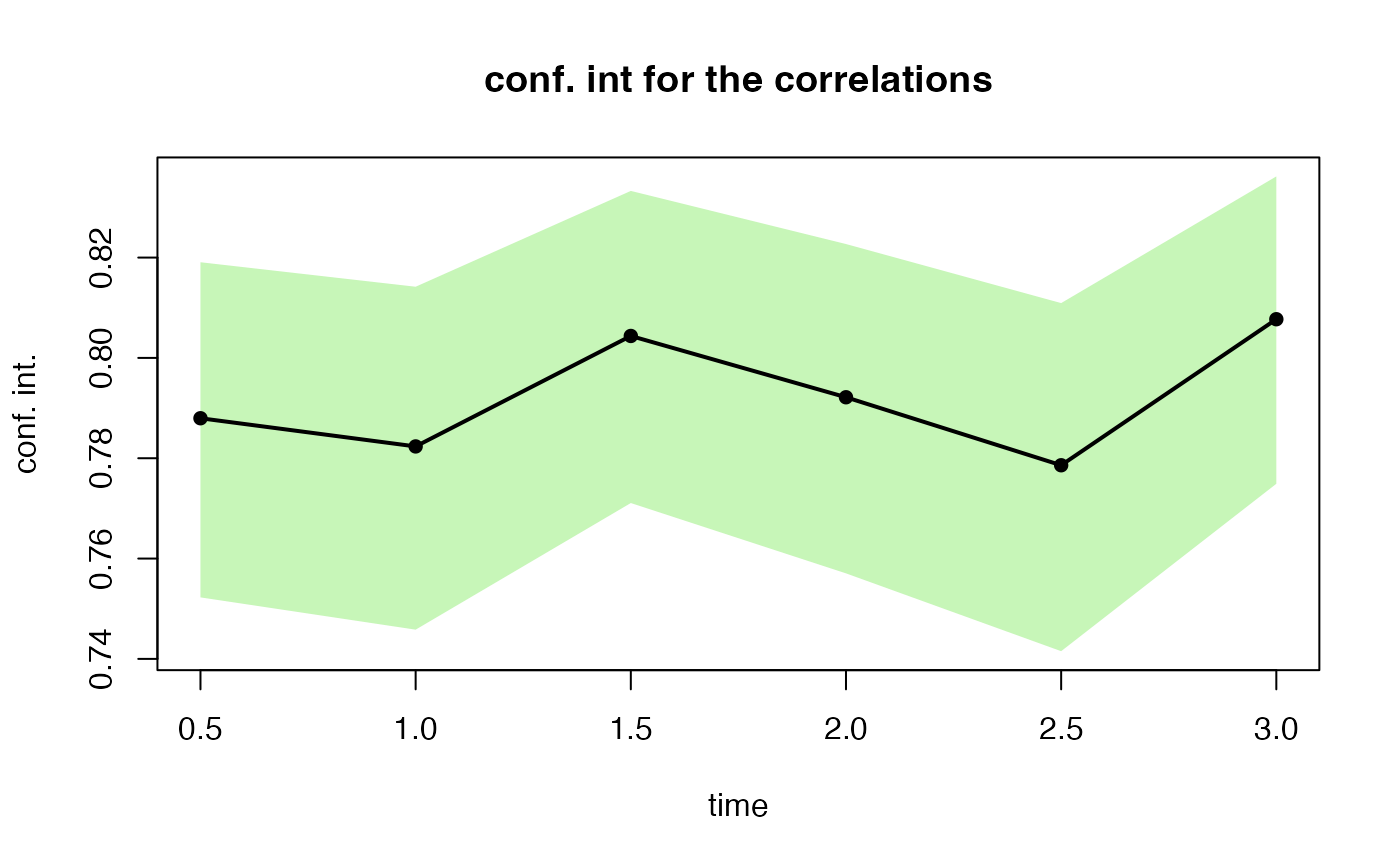

(test2 <- esgcortest(s0.par2))

#> $cor.estimate

#> Time Series:

#> Start = c(0, 2)

#> End = c(3, 1)

#> Frequency = 2

#> [1] 0.7879729 0.7823533 0.8043743 0.7921554 0.7786005 0.8077114

#>

#> $conf.int

#> Time Series:

#> Start = c(0, 2)

#> End = c(3, 1)

#> Frequency = 2

#> Series 1 Series 2

#> 0.5 0.7522620 0.8190677

#> 1.0 0.7458304 0.8141866

#> 1.5 0.7710721 0.8332881

#> 2.0 0.7570532 0.8226977

#> 2.5 0.7415392 0.8109245

#> 3.0 0.7749064 0.8361767

#>

#par(mfrow=c(2, 1))

esgplotbands(test1)

esgplotbands(test2)

esgplotbands(test2)