Prediction intervals for Loess forecasting (simulation-based)

ahead-loess-forecasting.Rmdahead is a package for univariate and

multivariate time series forecasting, with uncertainty

quantification (R and Python).

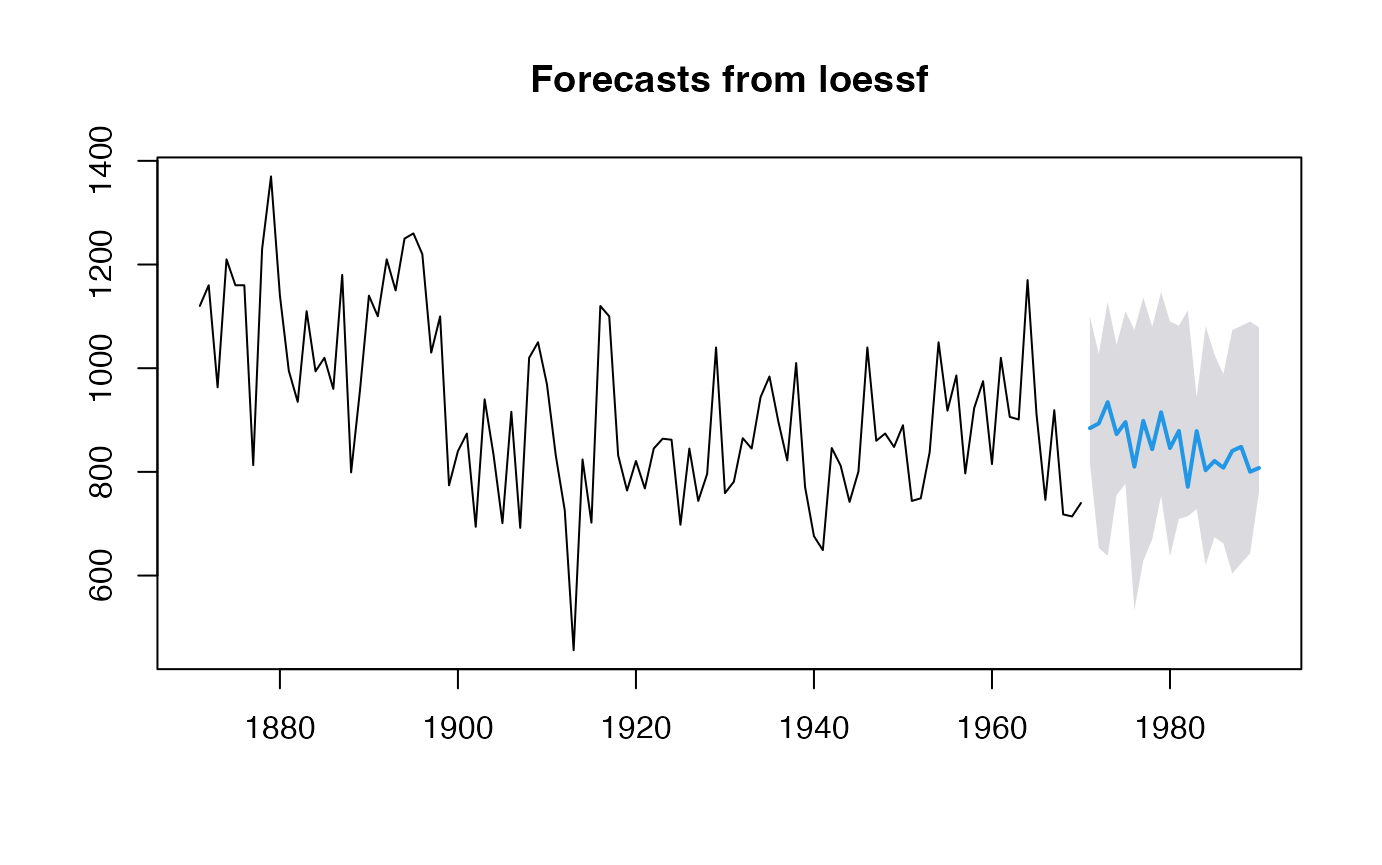

The model used in this demo is stats::loess (Local

Polynomial Regression Fitting), adapted to univariate

forecasting in ahead::loessf.

Currently for this model (as of 2023-08-28), for uncertainty quantification, options are:

- Independent bootstrap of the residuals

- Multivariate circular block bootstrap of the residuals

- Multivariate moving block bootstrap of the residuals

- Adjustment of a copula to the residuals

- More options to come in the future.

Please remember that in real life, this model’s hyperparameters will have to be tuned.

Install ahead

Here’s how to install the R version of the package:

-

1st method: from R-universe

In R console:

options(repos = c( techtonique = 'https://techtonique.r-universe.dev', CRAN = 'https://cloud.r-project.org')) install.packages("ahead") -

2nd method: from Github

In R console:

devtools::install_github("Techtonique/ahead")Or

remotes::install_github("Techtonique/ahead")

And here are the packages that will be used in this vignette: