Introduction to R package

ahead

ahead-vignette.Rmdahead is a package for univariate and

multivariate time series forecasting. Five forecasting

methods are implemented so far, as of October 13th, 2021.

-

armagarchf: univariate time series forecasting method using simulation of an ARMA(1, 1) - GARCH(1, 1) -

dynrmf: univariate time series forecasting method adapted fromforecast::nnetarto support any Statistical/Machine learning model (such as Ridge Regression, Random Forest, Support Vector Machines, etc) -

eatf: univariate time series forecasting method based on combinations offorecast::ets,forecast::auto.arima, andforecast::thetaf -

ridge2f: multivariate time series forecasting method, based on quasi-randomized networks and presented in this paper -

varf: multivariate time series forecasting method using Vector AutoRegressive model (VAR, mostly here for benchmarking purpose)

Here’s how to install the package:

-

1st method: from R-universe

In R console:

options(repos = c( techtonique = 'https://techtonique.r-universe.dev', CRAN = 'https://cloud.r-project.org')) install.packages("ahead") -

2nd method: from Github

In R console:

devtools::install_github("Techtonique/ahead")Or

remotes::install_github("Techtonique/ahead")

And here are the packages that will be used in this vignette:

Univariate time series

In this section, we illustrate dynrmf forecasting, with

Random Forest and SVM. Do not hesitate to type ?dynrmf,

?armagarchf or ?eatf in R console for more

details and examples.

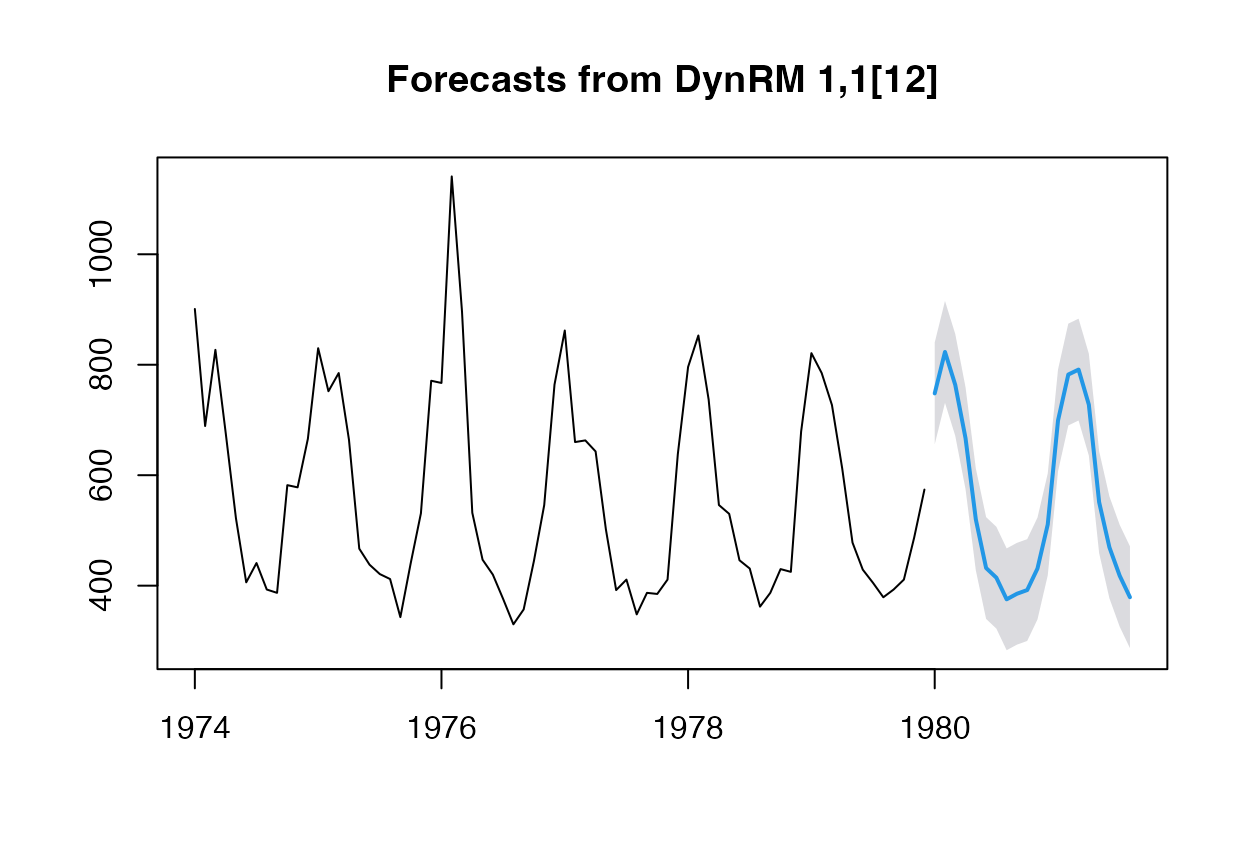

# Plotting forecasts

# With a Random Forest regressor, an horizon of 20,

# and a 95% prediction interval

plot(dynrmf(fdeaths, h=20, level=95, fit_func = randomForest::randomForest,

fit_params = list(ntree = 50), predict_func = predict))

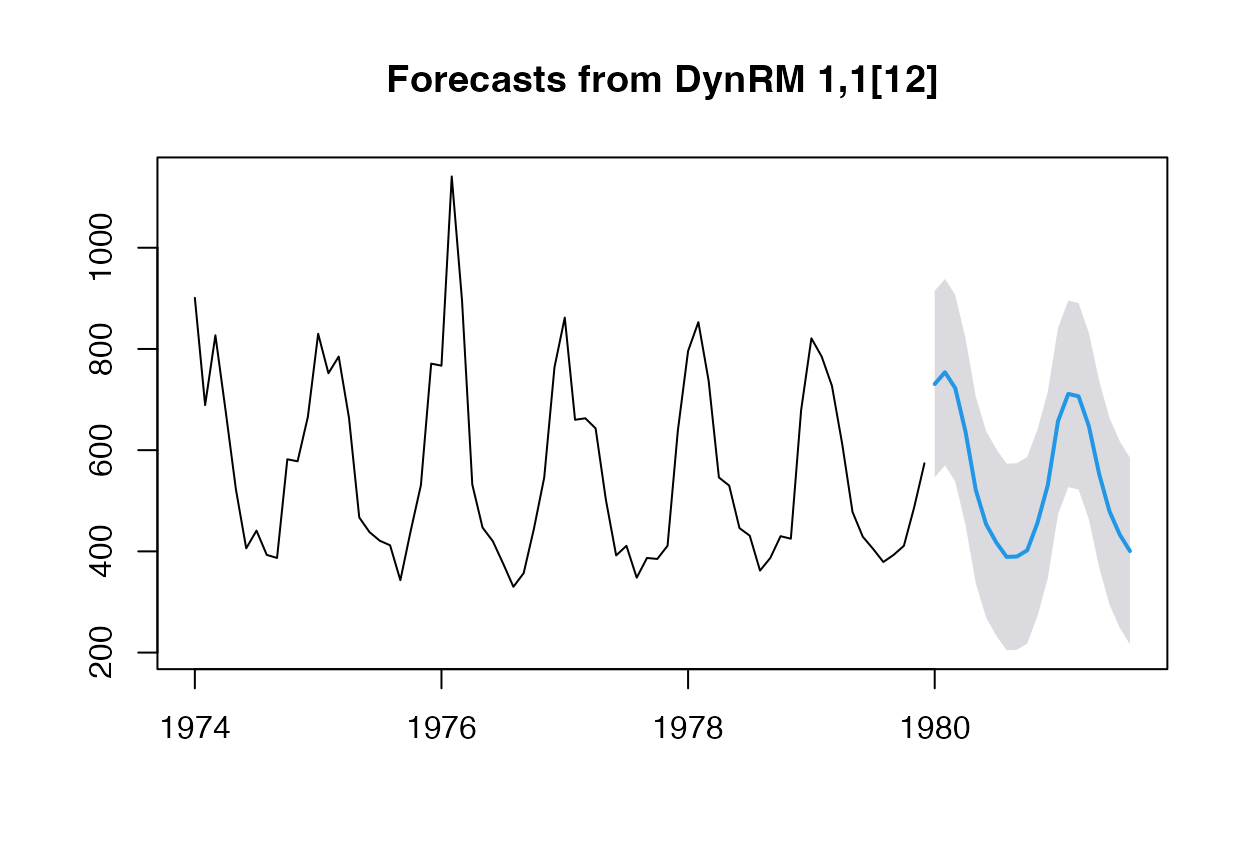

# With a Support Vector Machine regressor, an horizon of 20,

# and a 95% prediction interval

plot(dynrmf(fdeaths, h=20, level=95, fit_func = e1071::svm,

fit_params = list(kernel = "linear"), predict_func = predict))

plot(dynrmf(Nile, h=20, level=95, fit_func = randomForest::randomForest,

fit_params = list(ntree = 50), predict_func = predict))

plot(dynrmf(Nile, h=20, level=95, fit_func = e1071::svm,

fit_params = list(kernel = "linear"), predict_func = predict))

For more advanced examples on dynrmf, you can read this

blog

post.

Multivariate time series

In this section, we illustrate ridge2f and

varf forecasting. Do not hesitate to type

?ridge2f or ?varf in R console for more

details on both functions.

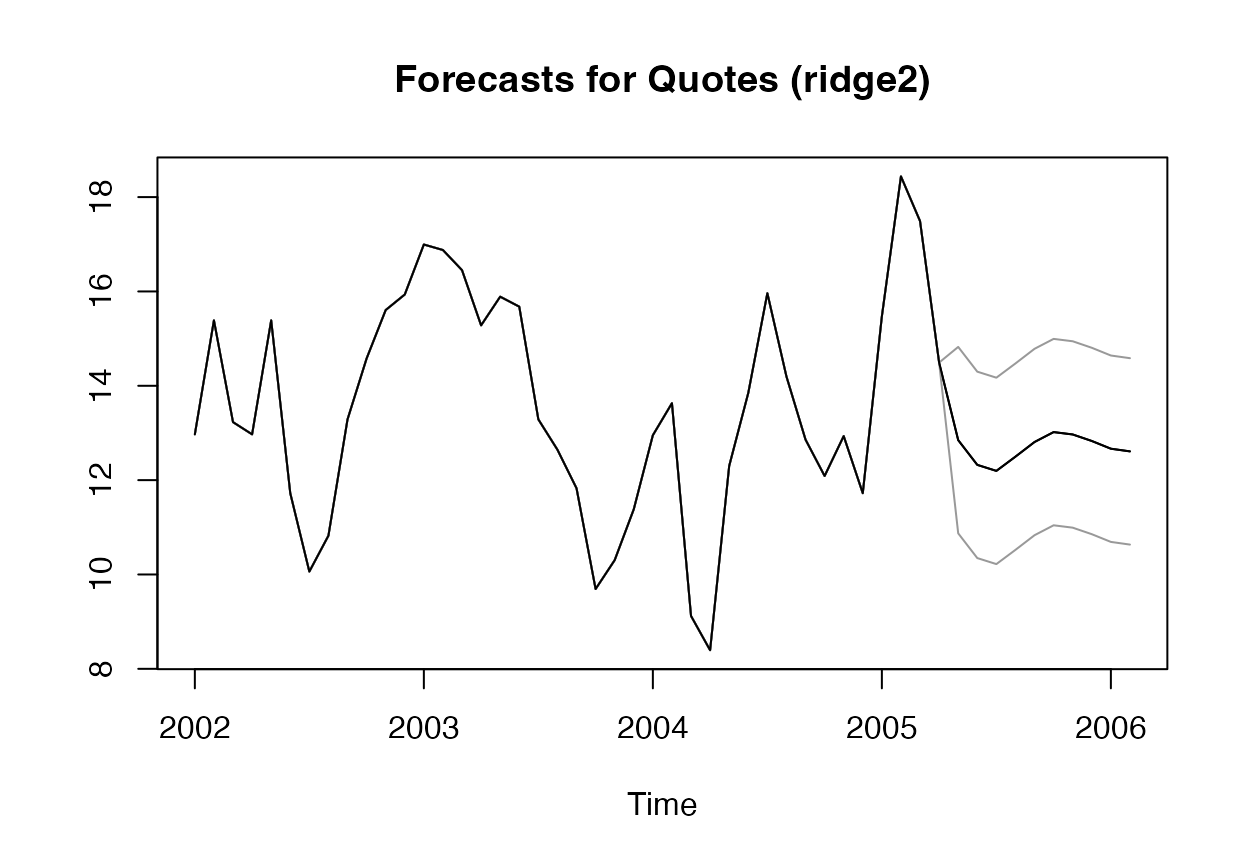

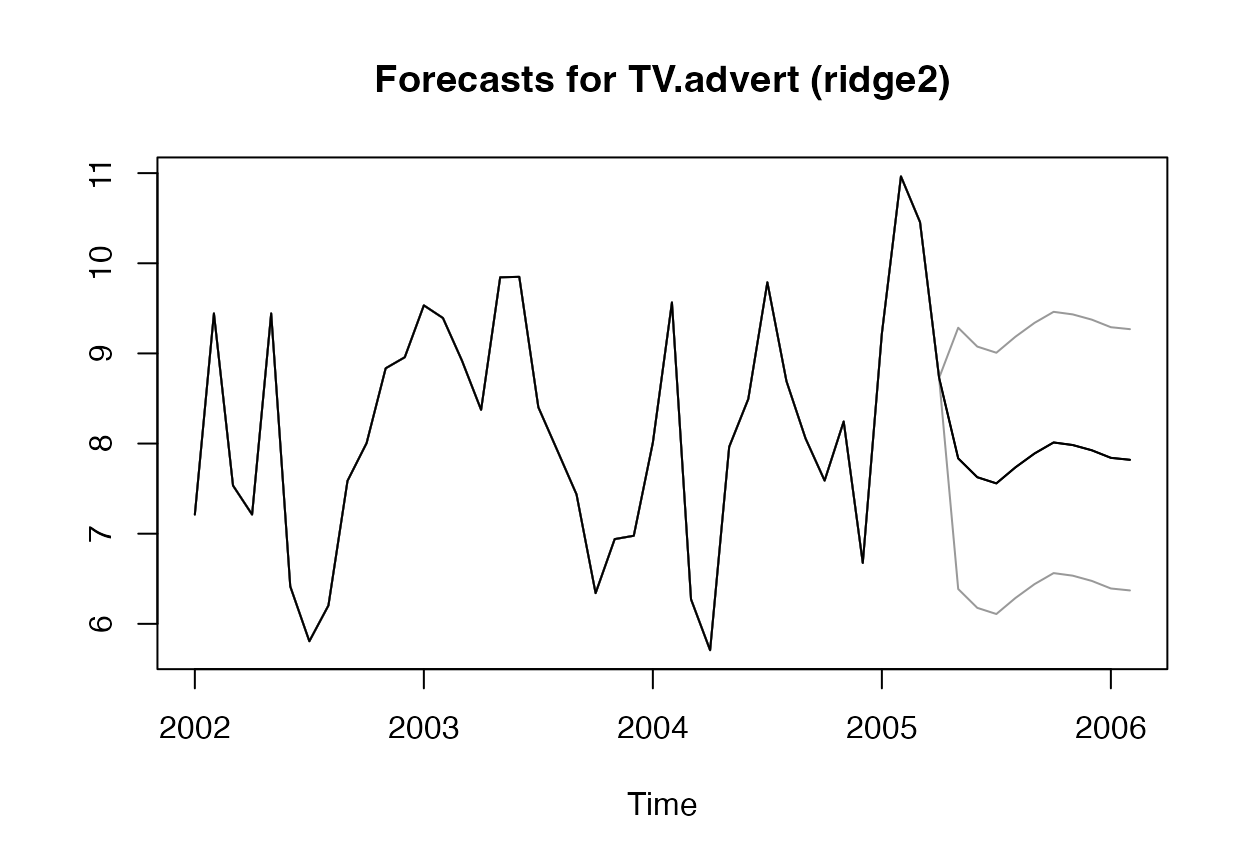

# Forecast using ridge2

# With 2 time series lags, an horizon of 10,

# and a 95% prediction interval

fit_obj_ridge2 <- ahead::ridge2f(fpp::insurance, lags = 2,

h = 10, level = 95)

# Forecast using VAR

fit_obj_VAR <- ahead::varf(fpp::insurance, lags = 2,

h = 10, level = 95)

# Plotting forecasts

# fpp::insurance contains 2 time series, Quotes and TV.advert

plot(fit_obj_ridge2, "Quotes")

plot(fit_obj_VAR, "Quotes")

plot(fit_obj_ridge2, "TV.advert")

plot(fit_obj_VAR, "TV.advert")